The Cost of “Doing it Yourself”: Hidden Risks of DIY Small Business Accounting

For many entrepreneurs, the “DIY” spirit is a badge of honor. When you’re starting out, every dollar saved feels like a victory, and handling your own books seems like a logical way to keep overhead low. After all, how hard can a few spreadsheets or a subscription to accounting software be?

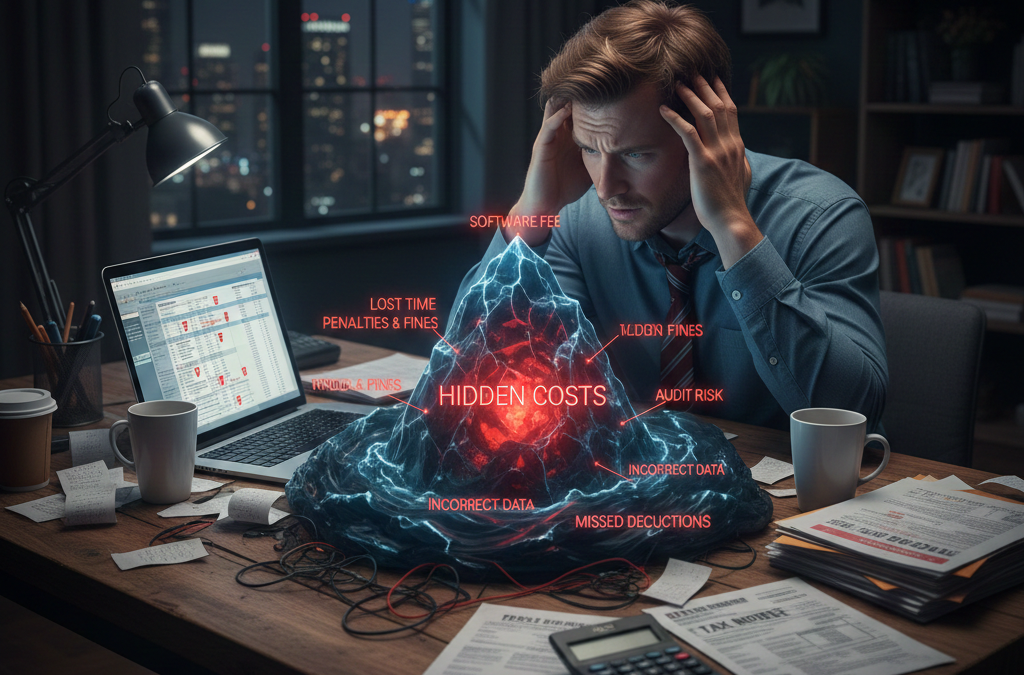

However, what starts as a cost-saving measure can quickly morph into a significant financial and operational drain. While DIY accounting looks free on the surface, the hidden risks often carry a much higher price tag than a professional’s fee.

The “Time is Money” Paradox

The most immediate cost of DIY accounting isn’t financial, it’s opportunity cost. Every hour you spend categorizing receipts, reconciling bank statements, or chasing down invoices is an hour you aren’t:

Developing new products.

Closing sales calls.

Scaling your operations.

If your billable rate is $100/hour and you spend 10 hours a month on messy bookkeeping, that “free” DIY approach just costs your business $1,000 in lost growth potential.

The Danger of “Unknown Unknowns”

Accounting software is a tool, not a professional advisor. It can help you record data, but it won’t tell you if you’re misclassifying assets or missing out on industry-specific tax credits. Common DIY pitfalls include:

Co-mingling Funds: Accidentally mixing personal and business expenses, which can pierce the “corporate veil” and leave your personal assets at risk.

Inaccurate Cash Flow Projections: Misunderstanding the difference between “money in the bank” and “actual profit,” leading to overspending at the wrong time.

Missing Deductions: Not knowing which home office, travel, or equipment expenses are actually deductible under current tax laws.

Compliance and the “IRS Anxiety”

Tax laws are not static; they are a moving target. Staying compliant requires constant monitoring of federal, state, and local regulations. A simple DIY error, like filing payroll taxes late or incorrectly calculating sales tax for out-of-state customers, can trigger:

Hefty Penalties: Interest and late fees that often exceed the original tax owed.

Audit Red Flags: Consistently messy books are an invitation for regulatory bodies to take a closer look at your entire operation.

Decisions Based on Bad Data

Your financial statements are the “dashboard” of your business. If the data entry is flawed, your dashboard is lying to you. Making a major hire or taking out a loan based on inaccurate profit margins is like flying a plane with a broken altimeter. By the time you realize the numbers were wrong, the damage is often already done.

There is a distinct difference between saving money and creating value. While DIY accounting might save a few hundred dollars a month today, the long-term costs of errors, missed tax breaks, and lost time can be devastating to a growing business.

Think of a professional accountant not as an expense, but as an investment in your infrastructure. They provide the clarity you need to stop working in your business and start working on it.

“We’ve confidently referred businesses to them, and the feedback has been unanimously positive.”

– Mike Doherty: Founder, Understanding eCommerce.

Follow us on LinkedIn – Zumifi.